DAMITT 2019 Year in Review: U.S. and EU merger review durations set records; Brexit in sight; DOJ vs. FTC trends

January 30, 2020

Fast Facts

United States

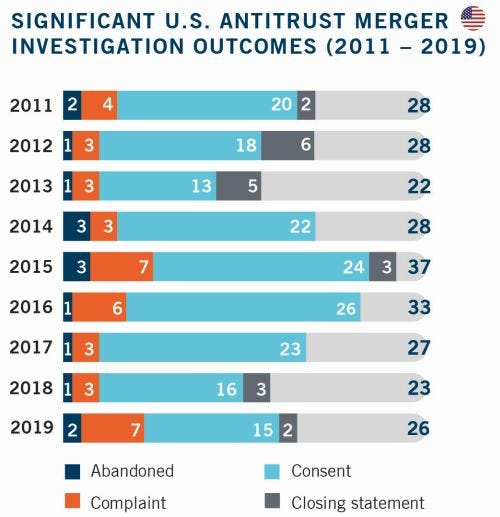

- The DOJ and FTC concluded 26 significant U.S. merger investigations in 2019 – similar to the level of activity from 2011-2014 under the Obama administration but trailing the activity observed during Obama’s final two years in office.

- The agencies filed seven complaints in 2019 seeking to block mergers – tying the record set in 2015 for the most in DAMITT’s nine-year history.

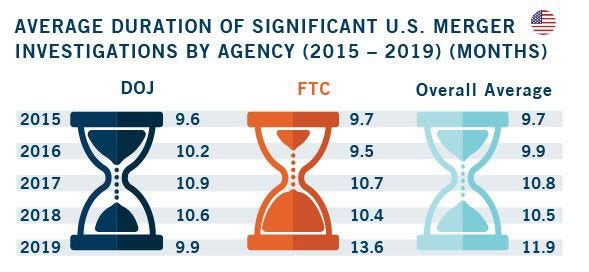

- The average duration of significant investigations increased to a DAMITT record of 11.9 months in 2019, despite agency calls in 2018 to streamline the merger review process.

- FTC-led significant investigations lasted an average of 37 percent longer (about four months) than those led by DOJ.

- The only U.S. DOJ or FTC merger litigation filed in 2019 and litigated to a decision (Evonik/PeroxyChem) was completed almost a month faster than similar cases over the prior three years and resulted in a rare litigation victory for the merging companies.

- Mergers with technology aspects attracted considerable attention from the U.S. agencies in 2019, accounting for nearly 20 percent of all significant investigations – the highest percent for the sector in any year since 2011.

Europe

- The number of significant EU investigations fell from 29 in 2018 to 19 in 2019. This was the fewest number of significant investigations since 2014.

- The total number of mergers notified to the EU was 382, down from 414 in the previous year.

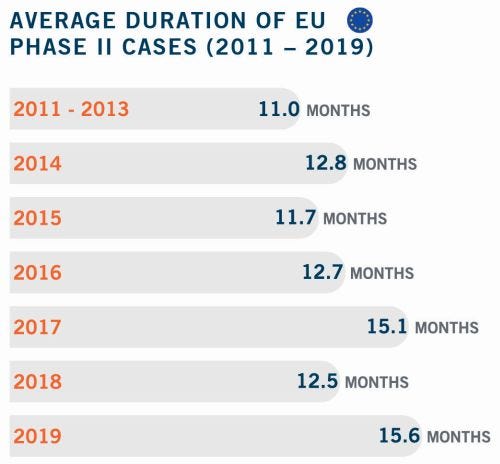

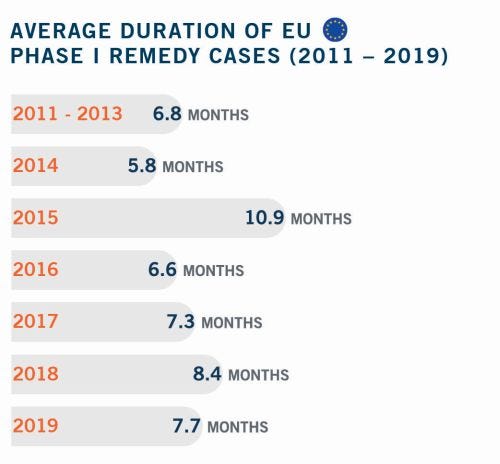

- Duration results were mixed in 2019 compared to 2018. Cases proceeding to Phase II lasted nearly 25 percent longer at an average of 15.6 months, a new record high over the 2011-2019 period tracked by DAMITT. Phase I remedy cases were completed eight percent faster than in 2018, at an average of 7.7 months.

- Three Phase II cases were blocked, the highest number of prohibitions for any year in DAMITT history. But this result does not necessarily reflect increased enforcement vigor given that the blocked transactions reportedly involved highly concentrated industries.

The Dechert Antitrust Merger Investigation Timing Tracker (DAMITT) is a quarterly release from Dechert LLP’s Antitrust/Competition practice reporting on trends in significant merger control investigations in the United States (U.S.) and European Union (EU).

In the U.S., “significant” merger investigations include Hart-Scott-Rodino (HSR) Act reportable transactions for which the result of the investigation by the Federal Trade Commission (FTC) or the Antitrust Division of the Department of Justice (DOJ) is a consent order, a complaint challenging the transaction, an official closing statement by the reviewing antitrust agency, or the abandonment of the transaction with the antitrust agency issuing a press release.

In light of the procedural differences between the EU and U.S., DAMITT defines “significant” EU merger investigations to include transactions subject to the EU Merger Regulation and resulting in either a Phase I remedy or the initiation of a Phase II investigation.

DAMITT calculates the durations of significant investigations in both jurisdictions from the deal announcement date until the completion of the investigation, and therefore includes the time attributable to pre-notification consultation efforts.

Duration of Significant U.S. Merger Investigations Rises in 2019 Despite Agency Calls for Reform

Despite early signs that the Trump Administration had begun to reverse the trend toward longer significant investigations, the average duration increased in 2019 to a record high of 11.9 months over the 2011-2019 period tracked by DAMITT. In 2018 – the first full year of President Trump’s administration – DAMITT observed the first and only annual decline in the average duration of significant merger investigation reviews, from 10.9 months in 2017 to 10.5 months in 2018. The average duration of significant investigations in 2019, however, is now 20 percent longer than the 9.9-month average in 2016, President Obama’s final full year in office.

The median significant investigation duration for 2019 was 9.8 months, an increase from the 9.3-month median in 2018 and second only to the DAMITT record median of 9.9 months in 2015.

The disparity between 2019’s 11.9-month average and 9.8-month median was the largest in DAMITT’s nine years of data. This result was driven in part by a record-setting number of significant investigations at the high end of the range. In 2019, six significant investigations (about 23 percent) lasted more than 15 months – the highest number and percentage of significant investigations for any year since DAMITT started tracking. From 2011 to 2014, only one significant investigation lasted more than 15 months. Significant investigations topping 15 months became more frequent as of 2015, occurring four times on average each year from 2015-2019.

U.S. Significant Investigations Completed by FTC Took Longer on Average than Those by DOJ

Although the DOJ and FTC completed nearly the same number of significant investigations in 2019, the average FTC significant investigation took nearly four months longer than those conducted by DOJ. For 2019, significant merger investigations conducted by DOJ lasted an average of 9.9 months with a median of 9.2 months, while investigations handled by FTC averaged 13.6 months with a median of 12.1 months. Five of the FTC’s significant investigations lasted more than 15 months, compared to only one for DOJ.

The 37 percent difference in durations between the FTC and DOJ significant investigations in 2019 was the largest between the agencies for any year in DAMITT’s nine-year history. By comparison, over the 2011-2018 period, the average durations of FTC and DOJ significant investigations were nearly identical – only 1.2 days apart.

U.S. Merger Litigation Duration Similar to 2016-2017 but Slower than 2018

The FTC’s lawsuit to block Evonik/PeroxyChem – the only U.S. merger challenge filed in 2019 that was litigated to a decision – reached a verdict 176 days after the filing of the FTC’s complaint. This timeline was about a month faster than the 207-day and 203-day averages for 2016 and 2017, respectively. However, the Evonik litigation lasted almost a month longer than the 149-day Wilhelmsen/Drew Marine FTC litigation in 2018.

Notably, although DAMITT only tracks significant investigations initiated by one of the federal antitrust agencies, state attorneys general sued to block the Sprint/T-Mobile merger before the DOJ announced a settlement requiring a substantial divestiture to Dish Network. The time from the filing of the Sprint/T-Mobile complaint to the end of the 10-day trial was 193 days, 81 days longer than Evonik/PeroxyChem, and over 60 days longer than the average trial length in 2017. The fact that the state attorneys general filed the Sprint/T-Mobile complaint prior to the completion of the DOJ’s review likely contributed to the longer period because, at the time the lawsuit began, the settlement had not been reached and closing was not imminent given the pending DOJ process.

Duration of Phase II EU Investigations Reaches 15.6-month Record; Phase I Remedy Case Duration Decreases Slightly from 2018

The average duration of Phase II proceedings concluded in 2019 reached 15.6 months, beating the 2017 record high of 15.1 months, and lasting more than three months longer than the 2018 average of 12.5 months and the 2011-2018 annual average of 12.1 months. Phase I remedy cases lasted an average of 7.7 months, nearly 10 percent shorter than the 2018 average of 8.4 months but still above the 2011-2018 average of 7.5 months. The average durations observed in 2019 are more in line with 2017 levels, when the average durations were 7.3 months for Phase I remedy cases and 15.1 months for Phase II proceedings.

EU Phase II Proceedings

Phase II proceedings resolved in 2019 averaged 15.6 months, more than three months longer than the 2018 average of 12.5 months. As observed in the DAMITT Q2 2019 and Q3 2019 reports, this increase likely was driven in part by the four complex Phase II investigations resolved during that period, in which the average duration exceeded 18 months. Moreover, four transactions were cleared unconditionally in the previous year, so that 2018 provides a low benchmark for comparison. Nevertheless, there has been a steady increase in the duration of Phase II investigations over the nine-year period tracked by DAMITT, with the average duration of investigations increasing by 61 percent.

The increase in the average duration of Phase II investigations is partly attributable to the increase in the average time in the pre-notification period. In 2019, the average time between the announcement and notification of Phase II transactions was 7.7 months. This is nearly two months longer than the 2018 average of 5.8 months and more than two months longer than the 2011-2018 average of 5.3 months. As explained in more depth in the DAMITT Q3 2019 report, pre-notification contacts have been a longstanding feature of EU merger reviews: merging parties invariably institute pre-filing talks with DG Competition staff very shortly after transaction announcement, if not before. The recent uptick in the period between announcement and notification is mostly explained by the EU Commission’s increased focus on internal company documents, which has contributed to merging parties spending more time and resources on pre-filing contacts.

DAMITT also observed an increase in the average duration of the “formal” review period, i.e. from notification to decision. In 2019, the average duration of the formal review period was 7.9 months, 18 percent longer than the 2011-2018 average. The average duration in the three previous years was relatively constant at approximately 6.7 months. This higher 2019 number reflects the EU Commission’s extensive use of its powers under Article 10(4) of the EU Merger Regulation to “stop the clock,” the most extensive over the 2011-2019 period tracked by DAMITT. The proportion of Phase II investigations hit with such orders in 2019 was 78 percent, adding an average of 0.9 months to each affected investigation. This observation is consistent with the steady increase in the EU Commission’s use of this procedural tool in the last four years (33 percent in 2016, 40 percent in 2017 and 50 percent in 2018). The previous high of 71 percent was set in 2014.

In addition, Article 10(3) of the EU Merger Regulation allows merging companies to grant “voluntary” extensions of time. These extensions are commonly conceded by merging parties at the urging of staff. All Phase II investigations concluded in 2019 entailed the use of such extensions, adding the statutory maximum 20 working days to the investigation period in all but one case. This is consistent with the pattern of the maximum possible extension being invoked since 2011, the first year tracked by DAMITT.

EU Phase I Remedy Cases

On average, Phase I remedy cases that concluded in 2019 lasted 7.7 months, down eight percent from the 2018 average of 8.4 months but up two percent from the 7.5-month average over the 2011-2018 period tracked by DAMITT. The drop in the average duration is mirrored in the duration of pre-filing talks. The average duration from announcement to notification in Phase I with remedy cases was 5.9 months in 2019, down 10 percent from the 2018 average but up three percent from the 5.8-month average over the period tracked by DAMITT. Phase I investigations resolved with remedies now tend to require more than five times the theoretical duration of the fixed timetable under the EU Merger Regulation.

U.S. Agencies Filed Record Number of Complaints Seeking to Block Mergers in 2019, but Significant Investigations with Vertical Aspects Declined

Number of U.S. Significant Investigations

The numbers show relative stability across Republican and Democratic-led administrations in terms of the volume of significant merger investigations.

The DOJ and FTC concluded 26 significant U.S. merger investigations during 2019. The data show that the U.S. agencies were almost equally aggressive in merger enforcement during 2019.

The FTC completed 14 significant investigations compared to 12 for DOJ.

Four of the FTC’s significant investigations resulted in a complaint seeking to block the merger, compared to three for DOJ.

Overall, the Trump Administration has averaged 25 significant investigations per year over the past three years. This result is similar to the 26.5 average during the 2011-2014 period under the Obama administration, but behind the totals for Obama’s final two years in office – 33 in 2015 and 37 in 2016.

The Trump administration has also been active in seeking to block mergers at a record rate. In 2019, the agencies filed seven complaints seeking to enjoin mergers, tied with 2015 for the highest number observed by DAMITT. In addition, the antitrust agencies took credit for the abandonment of two significant investigations prior to the filing of a federal court complaint.

U.S. Significant Investigations with Vertical Aspects

Vertical merger issues were pushed into the spotlight in 2017-2018 with heavy antitrust scrutiny of blockbuster deals such as the CVS Health’s US$70 billion acquisition of Aetna and AT&T’s US$85 billion acquisition of Time Warner. Due to heightened interest in vertical theories and a lack of modern guidelines, this month the DOJ and FTC jointly issued for public comment proposed vertical merger guidelines.

The number of significant investigations involving vertical issues declined from five in 2018 to three in 2019. All three of these 2019 significant investigations – Fresenius/NxStage, UnitedHealth/DaVita Medical, and Staples/Essendent – concluded in the first half of the year and were handled by the FTC. The drop off in the second half of the year could be attributable to heightened scrutiny of vertical deals.

During the nine years tracked by DAMITT, significant U.S. investigations with vertical aspects have lasted 2.2 months longer on average than those without vertical aspects. In 2019, this difference swelled to nearly four months (15.3 months vs. 11.4 months). This disparity could be driven by the fact that vertical issues can be more complicated for the agencies to analyze, typically requiring more complex economic modeling and more datasets. The introduction of the new vertical guidelines is not expected to substantially impact this trend.

U.S. Significant Investigations Involving Technology Products and Services

In 2019, mergers involving technology products and services – ranging from airline booking platforms to hardware encryption modules, genetic sequencing systems, and more – attracted considerable attention from the U.S. agencies. The DOJ and FTC completed five significant investigations in this technology space in 2019, more than double the average per year from 2016-2018. Of these five significant investigations, the agencies filed complaints in federal court to block two, settled two with divestitures, and took credit for the abandonment of one other deal prior to the filing of a complaint. Overall, significant investigations of technology-related products accounted for nearly 20 percent of all significant investigations in 2019 – the highest proportion in any year since 2011.

Although this heightened interest in technology issues coincides with the FTC’s formation of a dedicated Technology Task Force in February 2019, four of these five significant investigations were completed by the DOJ. Given the FTC’s increased allocation of resources and allowing time for the task force to more closely examine U.S. technology markets, however, more FTC significant investigations could follow in 2020. In particular, the FTC’s task force is expected to focus on digital technologies, including “online advertising, social networking, mobile operating systems, and platform businesses.” DAMITT will continue to monitor the increased spotlight on the technology sector to assess the impact of the increased attention.

Number of Significant EU Investigations in 2019 Decreases to its 2014 Level

The EU Commission concluded 19 significant EU merger investigations in 2019, down nearly 35 percent from the previous year and below the yearly average of 20.9 significant investigations over the 2011-2018 period tracked by DAMITT. This is the lowest number of significant EU merger investigations since 2014.

The decrease reflects a 41 percent drop in the number of significant Phase I investigations concluded in 2019 with the EU Commission concluding only 10 such investigations. In addition, the EU Commission resolved nine transactions in Phase II, down 25 percent from the previous year but still nearly 10 percent above the yearly average of eight Phase II investigations over the period tracked by DAMITT. Six of these merger investigations were cleared with remedies. The remaining three transactions were prohibited. This is the highest number of prohibitions since DAMITT started tracking and – after the 2001 high of five prohibitions – represents the second-highest number of prohibitions (tied with 1996) since the EU Merger Regulation came into force in 1990.

The decrease in significant EU merger investigations does not appear to be due to any slackening of enforcement intent. Rather, the decrease potentially reflects the fact that fewer transactions were notified in 2019. There were a total of 382 EU notifications, a decrease of eight percent from the previous year’s record high of 414 notifications. This is the first decrease in the number of notifications received by the EU Commission since 2013. So the reducing levels of deal activity are potentially correlated with the reduction in the number of “significant” cases.

Almost 75 percent of the cases resolved by the EU Commission in 2019 were assessed under the short-form/simplified procedure. The average duration of the EU Commission’s review of those short-form cases, measured from notification to decision, was 17.6 working days. This is considerably below the maximum Phase I review period of 25 working days. The revised simplified procedure has been one of the most successful features of the 2013 overhaul of the EU merger control regime, resulting in a significant reduction in the time it takes the EU Commission to review cases that do not give rise to substantive issues.

The EU Commission also cleared unconditionally an acquisition in Phase I even though the parties had offered remedies, finding those remedies unnecessary. This is a rare occurrence and has only happened three times since the 2013 reform of the merger control regime.

Orderly Brexit Secured/No-Deal Brexit Averted For Now

Following the United Kingdom (UK) General Election on December 12, 2019, the government had the parliamentary majority it needed to enact its Brexit policy and secure an orderly exit from the EU. The EU (Withdrawal Agreement) Bill was adopted by the UK Parliament on January 22, 2020. The Bill will amend the EU (Withdrawal) Act to provide for an “implementation” (i.e., transition) period until December 31, 2020 which will begin on the date of the UK’s exit from the EU: 11.00 p.m. London time on January 31, 2021, midnight in Brussels. There will be a period of continuity during the transition period with the UK competition regime remaining tethered to the EU system. Although the UK will no longer be a Member State, it will still be treated as one for purposes of the EU Merger Regulation.

In practice, this means that the EU Commission will continue to hold exclusive jurisdiction over deals meeting the thresholds thanks to revenue achieved in the UK. For merger reviews that are already in progress at the end of the transition period, i.e., December 2020 or later, the Withdrawal Agreement makes provision for the EU Commission to retain exclusive jurisdiction over those cases. For cases initiated later, the UK will become a separate filing jurisdiction, with the likelihood of a UK filing being required in addition to an EU filing.

It remains to be seen whether the EU and UK will reach a new trade deal by the end of 2020. Without one the threat of a No-Deal Brexit remains at that stage, i.e. in the sense of a reversion to World Trade Organization rules. This should not however be disruptive to the allocation of jurisdiction in merger reviews.

Conclusion

While the circumstances of future antitrust-sensitive transactions may lead to results above or below DAMITT averages, 2019 statistics suggest that parties to the hypothetical average “significant” deal subject to review only in the U.S. would have to plan on approximately 12 months for the agencies to investigate their transaction, and another five to seven months if they want to preserve their right to litigate an adverse agency decision. Deal timetables for EU cases where the investigation is likely to proceed to Phase II need to account for an average lapse of 15-16 months from announcement to clearance.

Since the UK will remain de facto part of the EU merger review process throughout 2020, there is no reason to anticipate any related inflection in the volume of EU filings. DAMITT will return in due time to the prospects for the period post-2020.

Related Professionals